Applying the K.I.S.S. method in leases

October 27, 2019

“Keep it simple, stupid!” That hits home so often as I am reading leases.

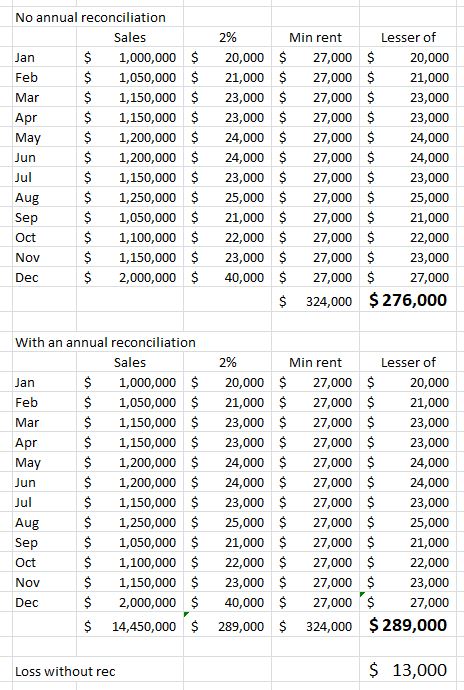

I have taught classes for ICSC for nearly 25 years. One of my favorite example has been base rents or fixed CAM charges increased by the CPI. That in and of itself is pretty simple. But, you often see caps on these increases, and in many cases where there are caps there are also floors. So the lease might read something to the effect of:

Minimum rent as reflected in Section x.x will be adjusted at the beginning of each Lease Year by the increase in the Consumer Price Index (CPI) from Index published as of the Commencement Date through the Index in effect as of the adjustment date. The increase applied shall never be less than 2% nor more than 4%. The Index shall be the CPI, Clerical Workers and Wage Earners, 1982-84=100 for the SMSA of which the property is apart.

This adjustment is not difficult to calculate, but it has so many different factors to consider.

- What is the Commencement Date? You might hone in on the Rent Commencement Date, but the Commencement Date might defined elsewhere as the Date of the Lease.

- What is the definition of Lease Year? Is it from the Commencement Date? Is it from the Rent Commencement Date? Is it 1/1-12/31? Is it 2/1-1/31?

- What is my SMSA? A property is midway between Philadelphia and DC? Do I go with Philly or DC? Do I go with Eastern Region?

- What is the “as of date”? It may sound silly, but “as of” Commencement Date is different that “for” the month of Commencement, which is different that Published “during” the month of Commencement. The possibility of three different months. And, the right index could change if the lease commenced on the 10th or 20th of the month (the Index is usually published mid-month, but it can be the 13th-17th).

- Are my floors (minimums) or cap (maximums) cumulative or non-cumulative?

Honestly, there are a handful of additional considerations.

However, with the idea of K.I.S.S., you can ask, what are we hoping to accomplish? Your minimum is 2%. Your maximum is 4%. Do we think maybe both parties are shooting for 3%? Is it possible they both have an idea of when each year they would like the increase to be applied?

So, instead of each year having to do the drawn out computation, it can be eliminated with:

Minimum rent will be increased by 3% each January 1 of the term, with the first increase effective 1/1/20.

No arguing of any component of a computation. Simple. Straightforward.

Why this post this week?

We are working on a portfolio acquisition and the seller has created some of the most complicated pools for one of these open air centers that I have ever seen. Grocery and discount store anchored. 11 different groupings for allocations. A similar number of pools within these groupings. Multiple denominators within each of these groupings. Caps. A Most Favored Nations clause or two.

And, there was one particular pool, with one particular denominator that had been created for one particular tenant. The total allocable expense in that pool? $158. Seriously, $158. The incremental pickup of creating the separate pool and the unique denominator? $1.30. That is not $1.30/sf. That is $1.30 total.

My life, and the lives of the professionals in our company (Meridian Realty Consultants), is about making sure that landlords do not leave any cash flow on the table. I can appreciate efforts to reduce a landlord’s absorption. But, the number of factors going in to that calculation – the expense coding, the allocation among the groupings, the denominators within the pools, the explanations necessary – all for $1.30?

I have a really bad tendency to associate scenes from movies or lyrics from songs to my current situation. As I wrote that $1.30, it brought back a scene from a movie I haven’t even thought about in probably 35 years. https://www.youtube.com/watch?v=e9mf3Bypyk8

Focus on what matters. And, K.I.S.S.